“This Just Makes No Sense”: European Regulators Rush To Calm AT1 Investors After Credit Suisse Wipeout Shock

— Sean Tuffy (@SMTuffy) March 20, 2023

- The AT1 (Additional Tier 1) bond market is about $250-275B in Europe. What the Swiss have done is re-write the rules of seniority in payment (ie. who get paid first). So, AT1 bond holders are now starting to react negatively by selling these AT1 bonds (in other financial institutions). Contagion is spreading. See:

–

What are AT1 bonds and why are Credit Suisse’s now worthless?

European bank supervisors step in to stem rout in bonds

AT1 Bond Rout Prompts European Officials to Try to Calm Market

–

- “This Just Makes No Sense”: European Regulators Rush To Calm AT1 Investors After Credit Suisse Wipeout Shock

by Tyler Durden, https://www.zerohedge.com/

14 years ago, the Obama administration (or rather his Wall Street lackey Steve Rattner) turned the bankruptcy process on its head with the Chapter 11 filing of General Motors, which steamrolled the bankruptcy liquidation waterfall by paying off the underfunded (and unsecured) pension plans of GM and Chrysler union workers at 40 cents on the dollar, while cramming down secured creditors, forcing them to accept 29 cents on the dollar in recovery.

–

On Sunday, something similar happened with Credit Suisse when, much to the shock of Europe’s $275 billion Additional Tier 1 market, some $17BN in Credit Suisse AT1, aka Contingent Convertible, bonds were wiped out even as equity holders received over $3 billion in consideration from UBS courtesy of Swiss taxpayers who ended up footing billions in contingent liabilities.

–

Not surprisingly, this morning the entire universe of riskiest bonds of European lenders – those in the AT1 tier – plunged after UBS agreed to buy the bank in a historic, government-enforced deal aimed at containing a crisis of confidence that had started to spread across global financial markets. It was the biggest loss yet for Europe’s AT1 market, which was created after the financial crisis to ensure losses would be borne by investors not taxpayers.

–

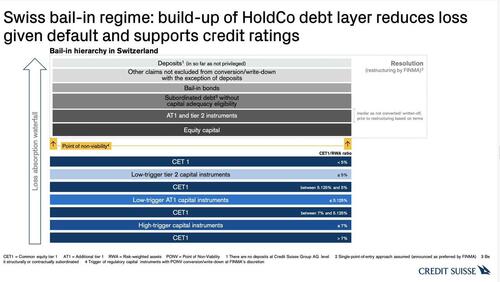

As shown in the Credit Suisse presentation chart below, in a typical writedown scenario, shareholders are the first to take a hit before AT1 bonds face losses. That’s why the decision to write down the bank’s riskiest debt — rather than its shareholders — provoked a furious response from some of the bondholders.

–

“This just makes no sense,” said Patrik Kauffmann, a fixed-income portfolio manager at Aquila Asset Management, who holds Credit Suisse CoCos. “Shareholders should get zero” because “it’s crystal clear that AT1s are senior to stocks.”

–

read more.

end